On this page

Regulation of the price of alcohol is the most cost-effective tool used by governments to address alcohol-related harm, according to the World Health Organisation. Governments use three main methods to regulate the price of alcohol:

- Varying alcohol prices

- Varying alcohol taxes/duties

- Using Minimum Unit Pricing (MUP)

This page includes figures on alcohol pricing in the UK, the level of taxation for each beverage type, how the price of alcohol affects both the level of consumption and the level of various harms, and the impact of different policy measures on those consumption and harms, including evidence in several countries.

Facts and stats

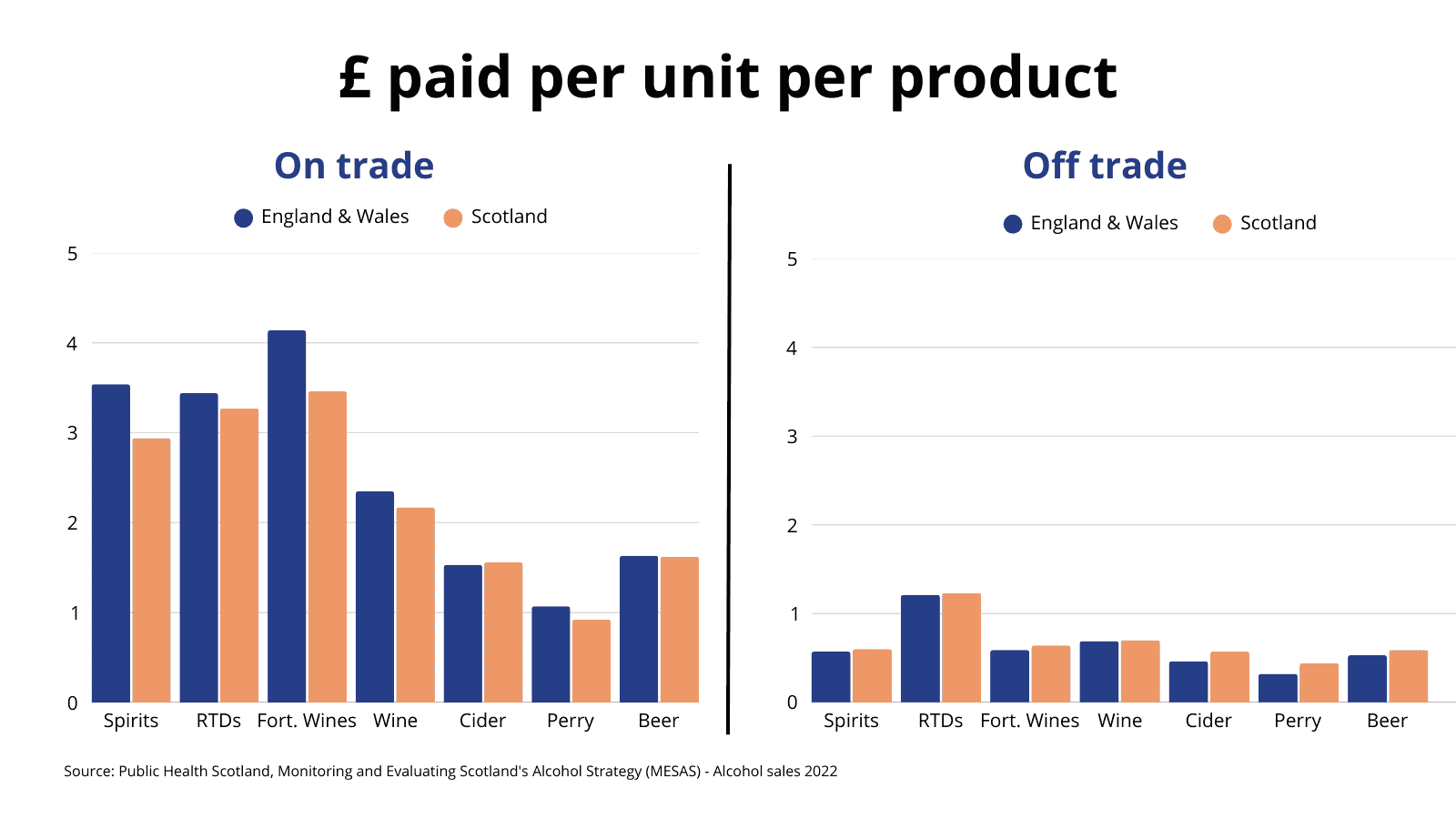

- The average 5% ABV pint of lager costs: £4.70 in the on-trade and £1.51 in the off-trade (ONS).

- 54p of the lager price is duty in the on-trade and 60p in the off-trade. This represents: 11% of the on-trade retail price; 40% of the off-trade retail price (duty rates).

- VAT is 20% of pre-tax price /17% of post-tax price. Excise duty varies between products, but on average accounts for around 25% of the final price. (Bhattacharya, 2017)

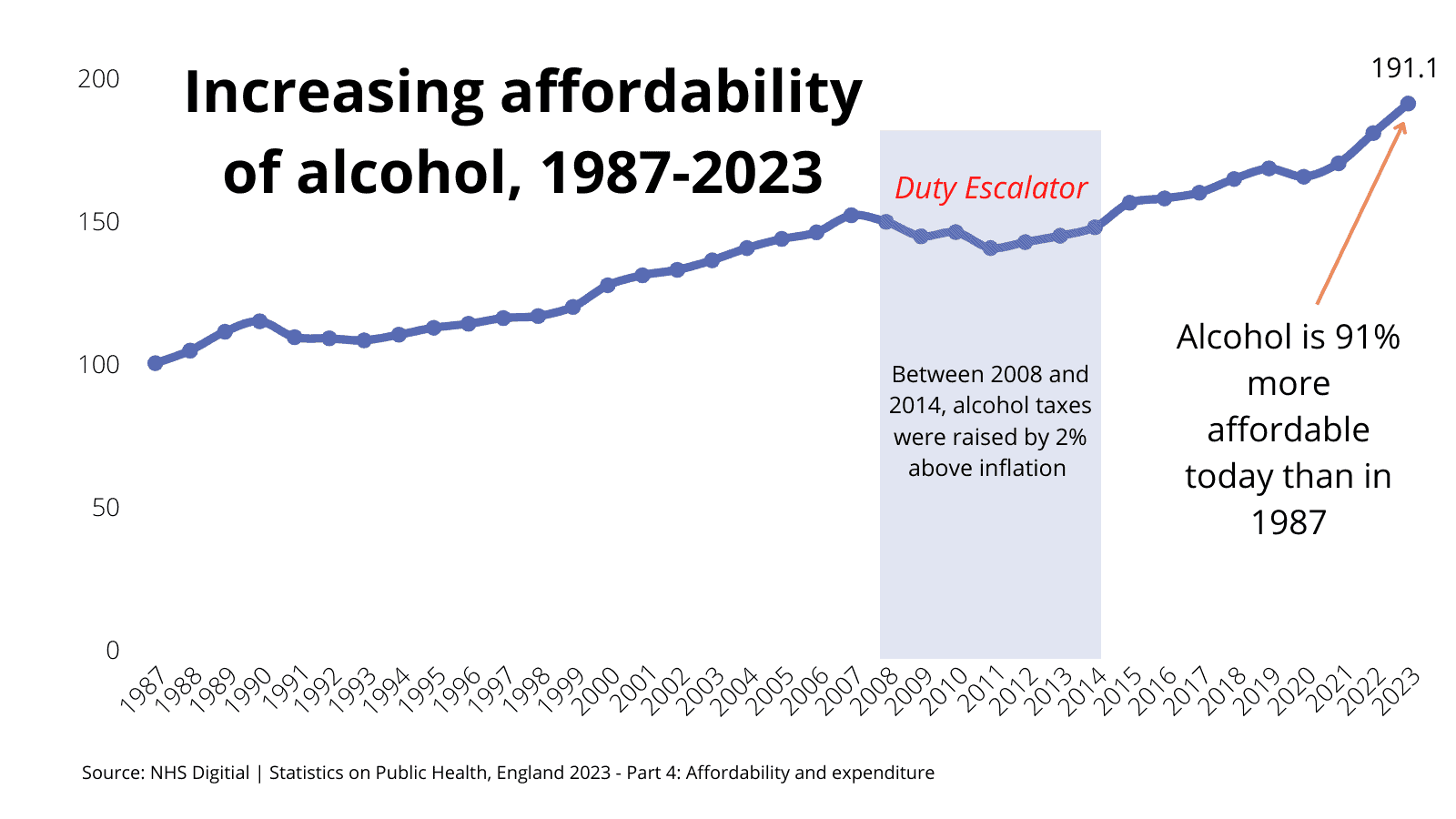

Affordability compared to 1987

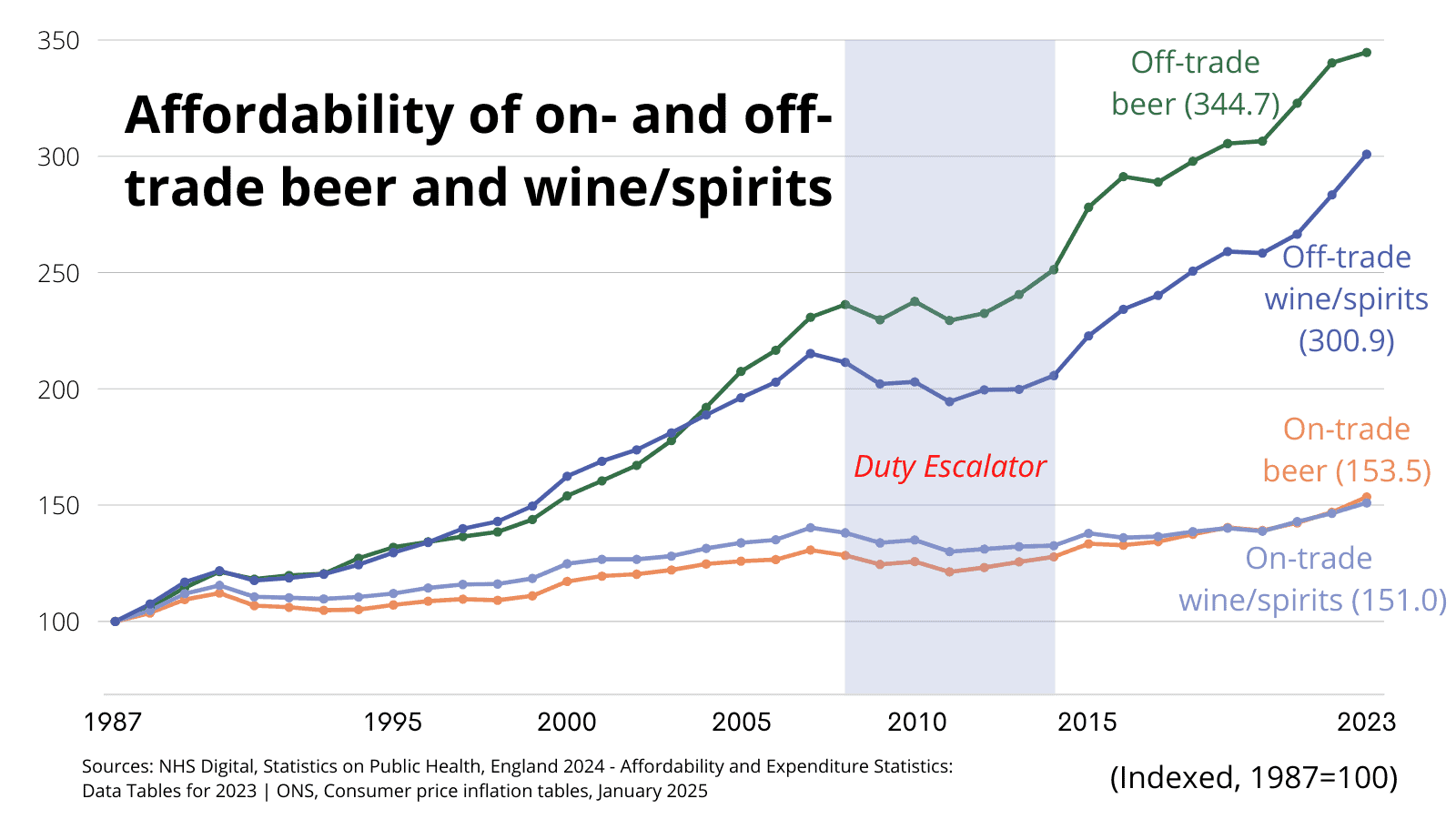

- Off-trade beer is 244.7% more affordable

- Off-trade wine/spirits is 200.9% more affordable

- On-trade wine/spirits is 51.0% more affordable

- On-trade beer is 53.5% more affordable

- The alcohol duty escalator increased duty by 2% above inflation each year between 2008-2013/14. This helped close the increasing gap between the cost of alcohol in the on- and off-trade, potentially helping the hospitality industry (see more here).

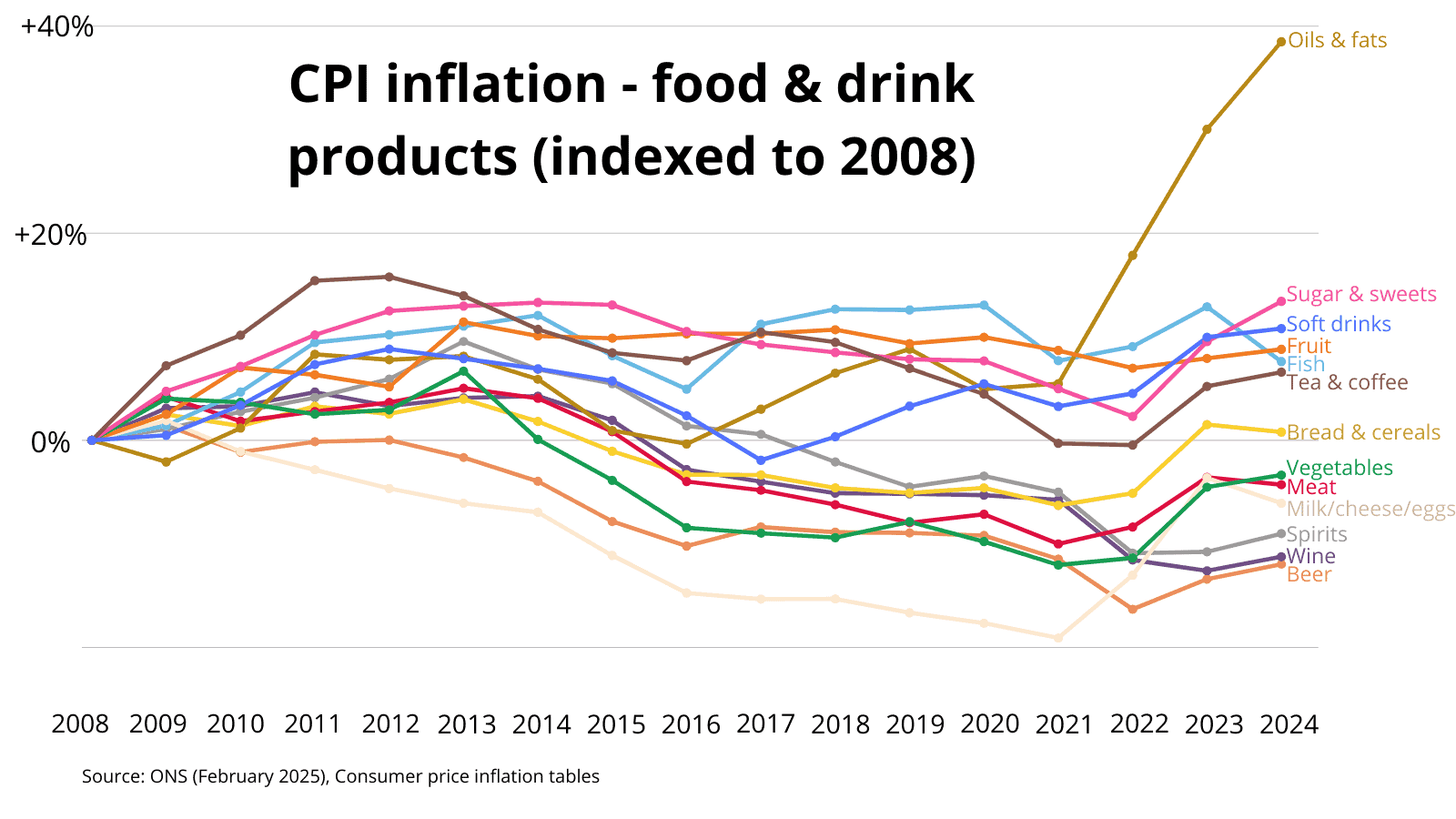

- The price of alcohol has not kept up with CPI inflation in recent years.

- Compared to all other food and drink products, alcohol has become the cheapest in real terms in recent years.

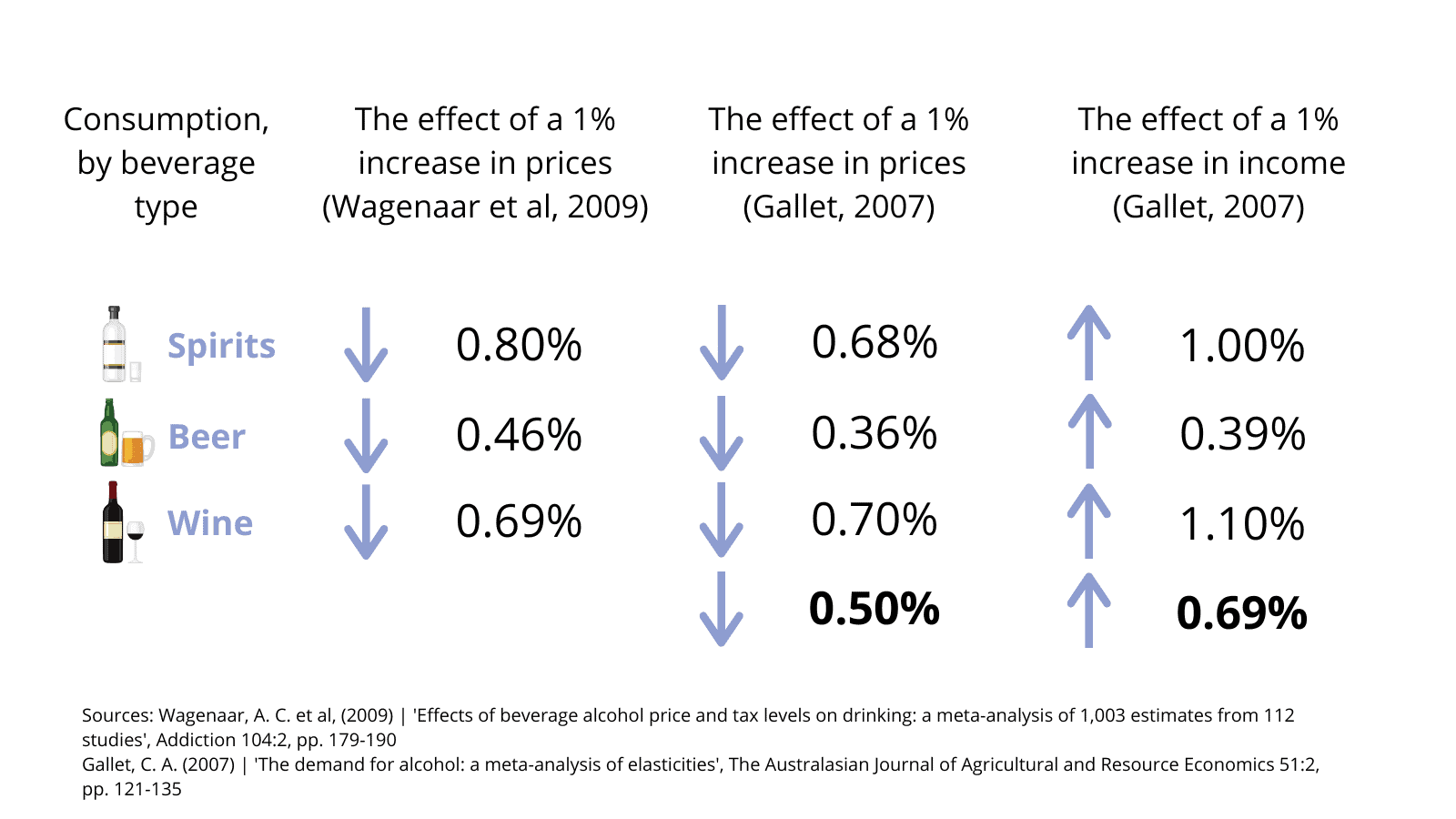

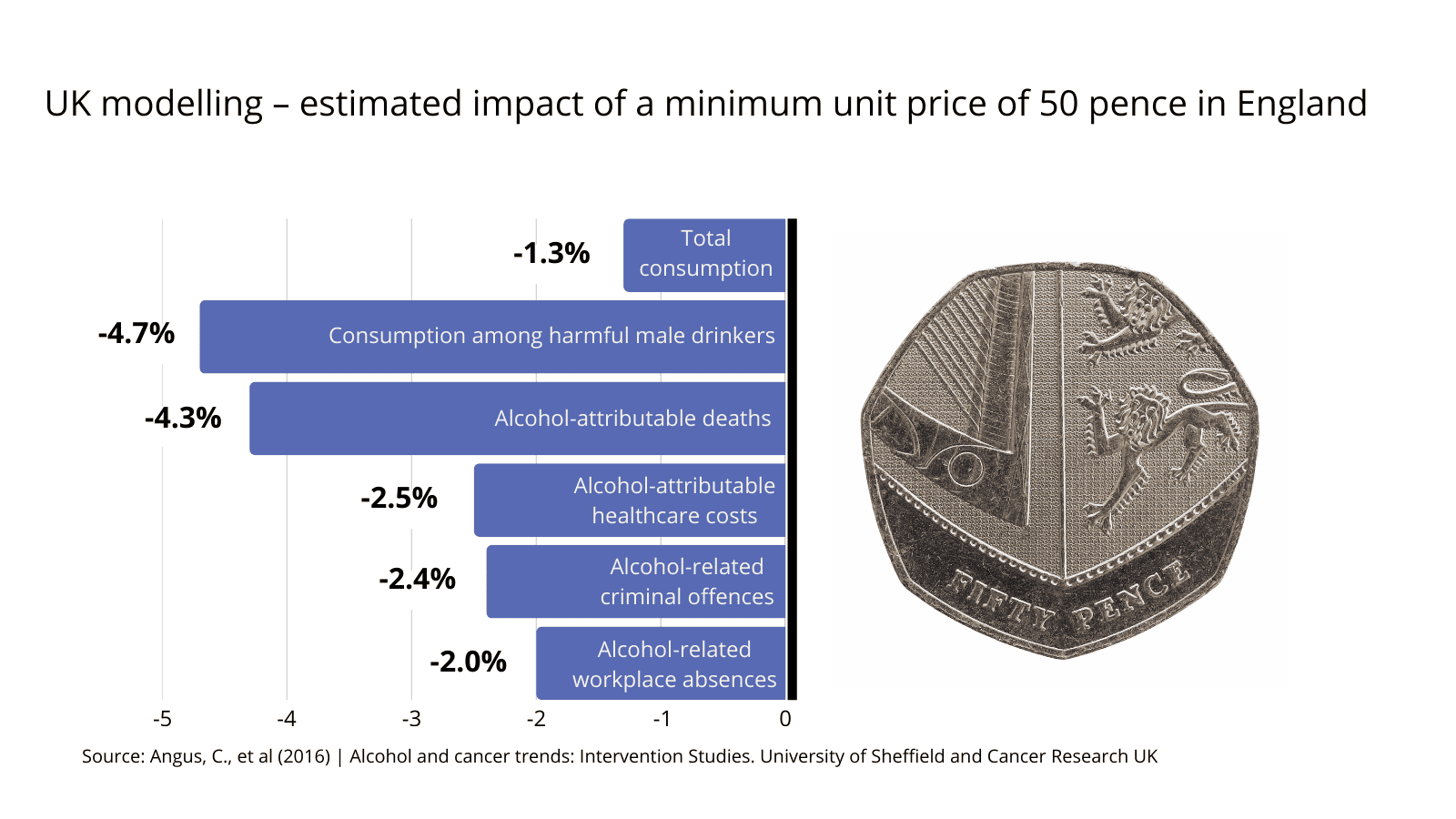

- As a rule of thumb, for every 1% increase in the price of alcohol, consumption falls by 0.5%

- Two major meta analyses each combining estimates from over 100 studies found:

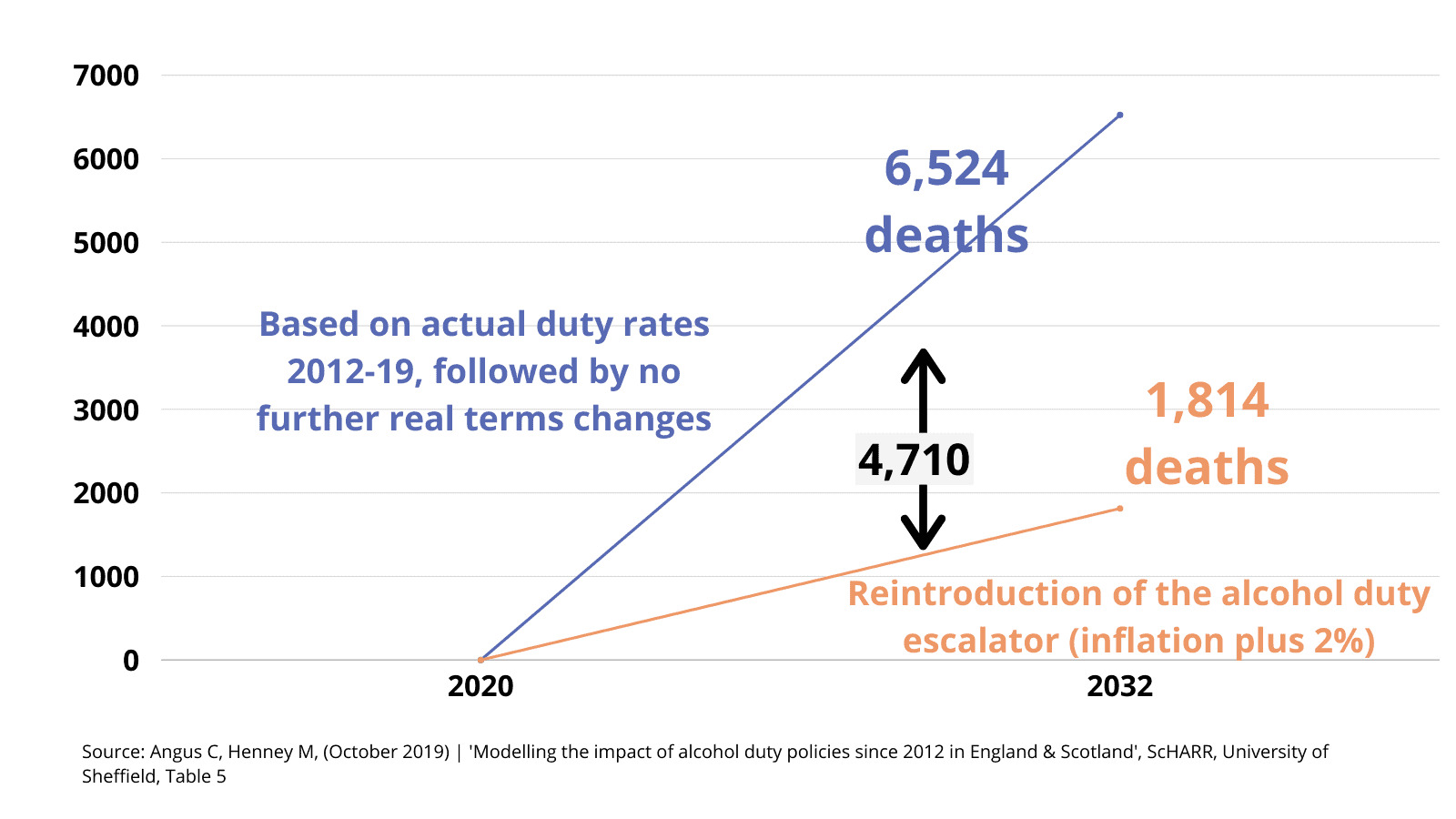

- If a duty escalator were introduced in 2020, an estimated 4,710 alcohol-attributable deaths would be averted by 2032, compared with a policy of increasing duties in line with inflation.

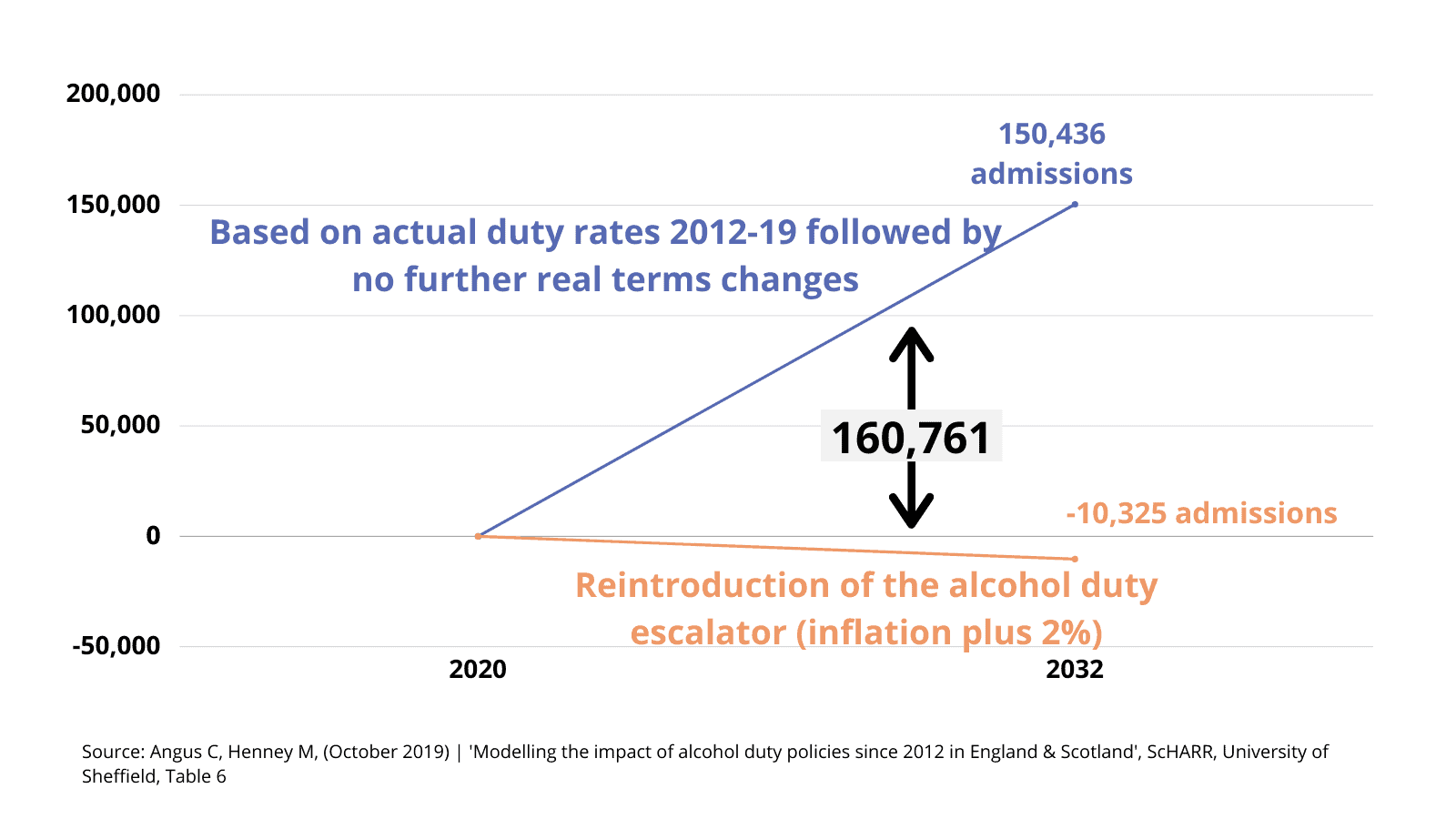

- If a duty escalator were introduced in 2020, an estimated 160,761 hospital admissions would be averted by 2032, compared with a policy of increasing duties in line with inflation

- Alcohol duty rates are supposed to increase in line with RPI inflation each year, so that they stay the same in real-terms.

- The current alcohol duty rates for 2025/26 can be found here, and were applicable from 01 February 2025.

- These will be increased by RPI inflation of 3.66%, with the new rates here.

- Nominal alcohol duty – so duty in cash-terms – has steadily increased over time (see first chart below).

- However, real-terms duty – so duty compared to inflationary increases of other products – is much lower now than in the past (see following chart).

- In real-terms, in 2026/27 compared to 2012/13:

- Beer duty is 32% lower

- Draught beer duty is 42% lower

- Cider and spirits duty is 26% lower

- Draught cider duty is 36% lower

- Wine duty is 19% lower

- Alcohol duty rates per litre of pure alcohol have steadily fallen in real-terms since 2012.

- The following chart particularly highlights ‘cider exceptionalism’, where cider is taxed at a far lower level compared to equivalent strength beer.

- It is generally agreed that higher strength alcohol such as spirits should be taxed at a higher rate per unit of alcohol, as these products are disproportionately consumed by higher risk drinkers.

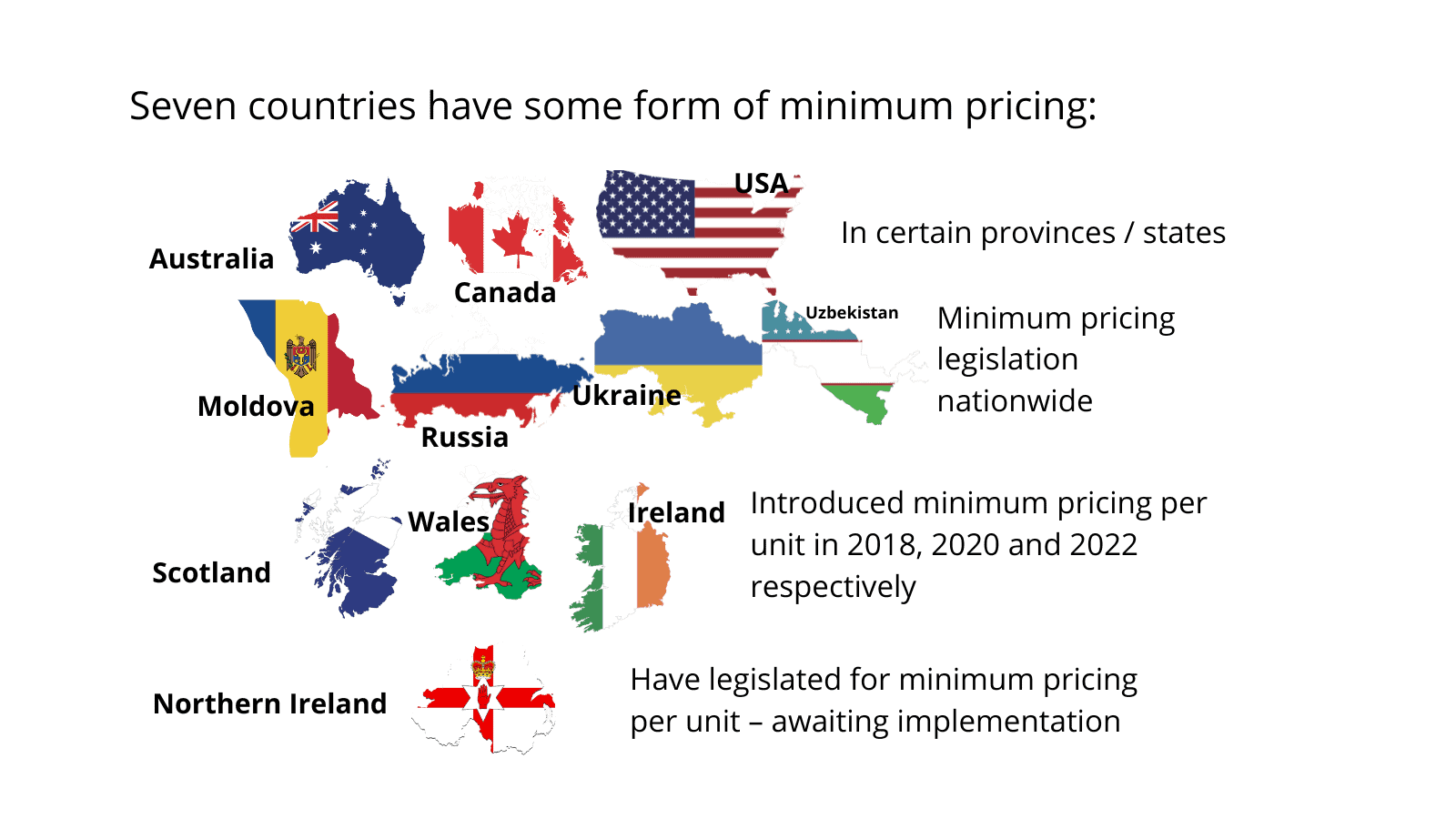

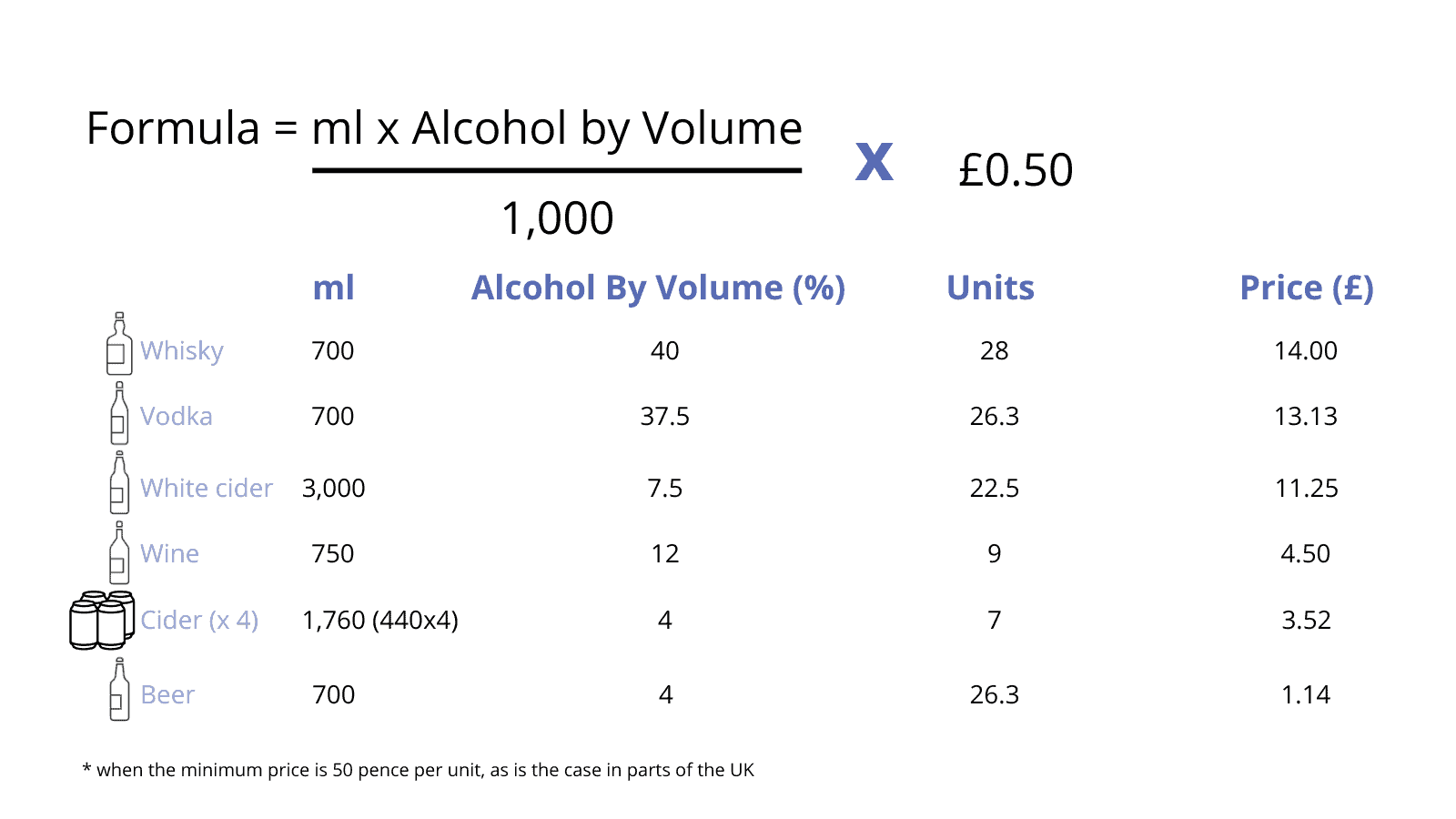

- Minimum alcohol pricing sets a ‘floor price’ below which alcohol cannot be sold. Under minimum unit pricing (MUP) the floor price is set according to the alcohol content of the drink, per unit.

- Minimum pricing is not a tax, and any additional revenue from raising prices goes to retailers rather than the government.

- In Scotland, MUP has reduced deaths wholly attributable to alcohol consumption by 13.4% – equating to 156 deaths every year. The greatest effects were seen amongst the four most socio-economically deprived areas. (PHS, 2023)

- Public Health Scotland found MUP to be associated with a net reduction of 3% in total per-adult sales of pure alcohol in the three years following implementation. (PHS, 2022)

- The reductions in alcohol purchases were greatest among households that were buying the most alcohol pre-MUP. (Wyper, Grant MA, et al. 2023)

- Although alcohol deaths have risen in every UK nation and region, they have risen far less in Scotland, partly due to minimum unit pricing.

- If the policy had not been in place, deaths would have risen far higher.

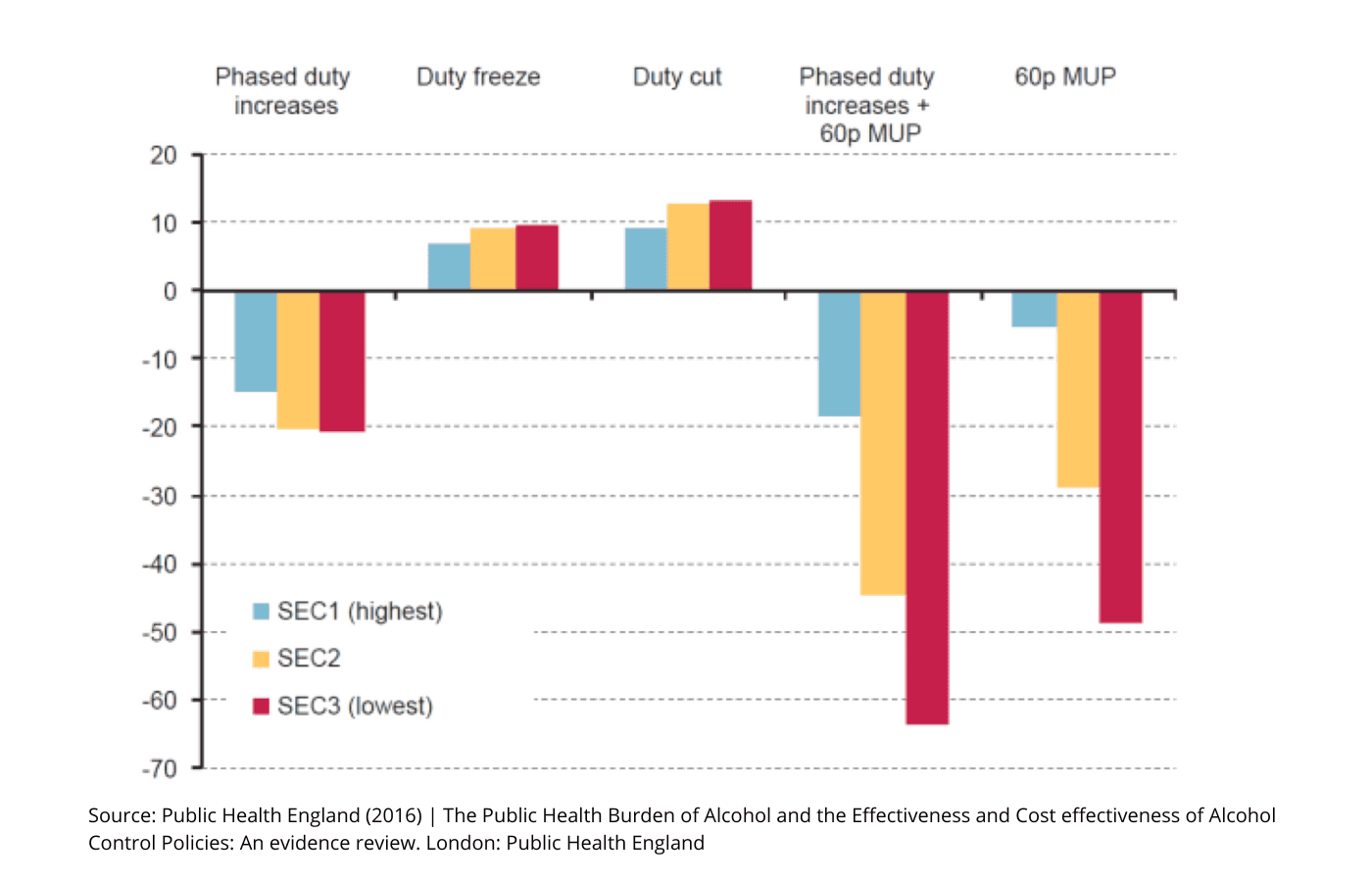

- Change in consumption at full effect by policy and socioeconomic status (units per year)

Briefings

Reports

Blogs

Is the Great British Pub on the verge of extinction? The truth behind the headlines

10th February 2026

Minimum unit pricing works – and it works for the people who need it most

18th December 2025

Budget 2025: Alcohol duty kept with inflation, but still far from true cost

16th December 2025

Why we need a long-term vision to tackle alcohol harm in the UK

11th November 2025

Who pays more? Analysing the impact of the UK’s 2023 alcohol duty reform

24th July 2025

Behaving irresponsibly: separating UK alcohol industry claims from reality

7th July 2025

We know MUP works – but we can make it even better

3rd June 2025

Policies that single out pregnant people’s drinking aren’t working, but there are other policies that appear to help

3rd April 2025

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}